For young people starting their careers in society, newlywed couples with their first sons, and middle-aged people who feel the burden of their work, the purchase of a new car in our society is something more than culture. Every day, new cars are massively launched in the marketplace. It is the era when, regardless of the country of origin for cars, there is fierce competition for new cars equipped with new technologies ranging from a change in the design of the car’s exterior to invisible details. The trends in the automotive industry have continuously developed over the past ten years, evolving from high performance cars to green cars such as electric cars, hybrid, and fuel-cell vehicles and to smart cars like autonomous cars. For the general public, such concepts are also well known to the point of predicting the future of vehicles.

However, from the perspective of technology, the future of both cars and the automobile industry in Korea is not that much brighter than people expect. Fortunately, Korea domestically produced major chemical materials by promoting the field of the heavy chemical industry in the early 1970s. With the world’s fifth-largest production based on chemical materials and original technology development project for chemical materials, Korea becomes a leader in the chemical materials industry. The future trends in the transportation industry are, as mentioned before, eco-friendly and smart. The most important factor is, at this point, an improvement in driving efficiency when a new power source is applied. Technically, the major issue is naturally the lightweight of materials used for transportation. Accordingly, if Korea systematically promotes industry sectors that integrate with the automobile industry by applying chemical materials in which Korea gained global competitiveness, it is likely to take the lead in the global market.

To maintain and expand the market share of domestic strategic industries, there is an urgent need to establish a virtuous circle in the ecosystem of the plastic-based chemical materials industry for transportation by improving technical skills in the domestic chemical materials industry through technical R&D promotion, fostering customized manpower for on-site work such as the chemical materials sector for transportation, and establishing infrastructure for the growth of SMEs. In this respect, this issue explores the trends in plastic-based chemical materials for transportation, the current status of the domestic and overseas market, the suggestions and problems of an industry ecosystem in Korea, and the directions and expected effects of R&D.

Evolving paradigm shift in the transportation industry

In the transportation industry, the major priorities are lightweight, functional, and eco-friendly technologies due to tightening regulations on fuel efficiency and carbon dioxide (CO2).

Such technologies are emerging as contributory factors for survival in the industry. In the case of vehicles, the standards of vehicle fuel efficiency in Korea will be 20km/L, which is significantly strict. The United States and the EU are also expected to tighten regulations.

In the case of shipbuilding, as the Energy Efficiency Design Index (EEDI) has required new ships to meet the standards since 2013, any ships failing to meet such standards can be prevented from sailing. As for aircraft, the EU will implement a law restricting CO2 emissions from aircraft engines.

The most effective way to respond to a new paradigm in the transportation industry is to improve engine performance; however, considering the pace of technical development and its costs, the realistic way is to develop high value-added chemical materials.

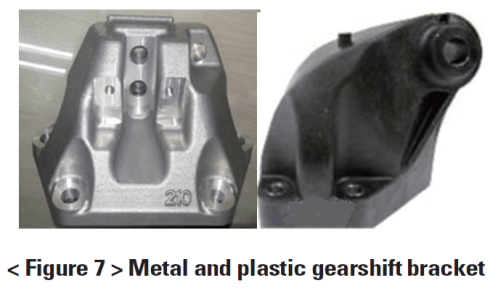

The conventional metal is strong and heat resistant, but in reality, it has limitations when responding to fuel economy regulations due to its heavy weight. High value-added chemical materials, such as engineering plastics, make it possible to be lightweight innovatively compared to metal components. They also can provide various functions, thus making it possible to streamline relevant parts. For these reasons, the transportation industry is gradually expanding from metal components to chemical materials in terms of the composition of materials.

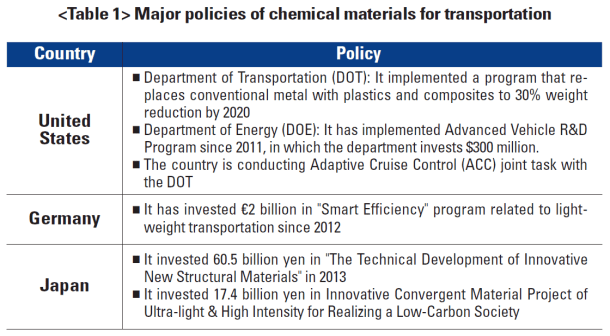

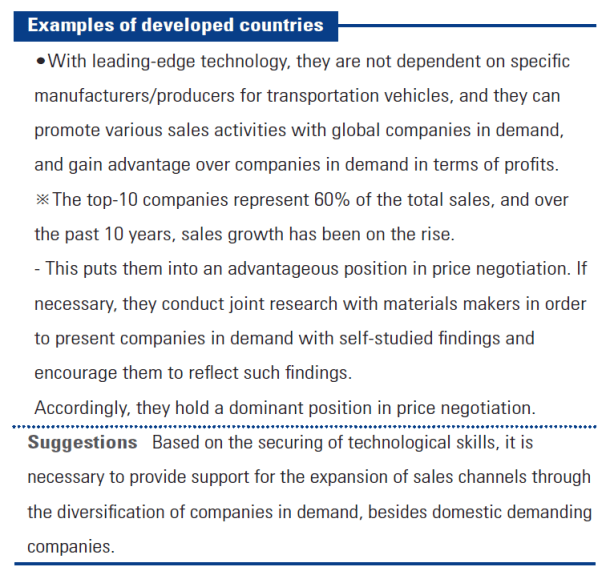

To respond to such environmental regulations and take the lead in the transportation industry, developed countries have implemented various policies by linking the chemical materials sector to the transportation industry. There are typical examples as follows:

In Korea, some efforts are made to respond to the rapid paradigm shift in the chemical materials industry. However, to lead such paradigm, there is a shortage of corporate size, R&D investment, domestic technology level, and infrastructure, so the government support is urgently needed. Companies specializing in chemical materials for transportation in Korea amount to a total of 2,400, among which 90% of the companies are small and medium-sized firms; the automotive component sector is about 880, among which 80% of the sector consist of SMEs and middle-standing firms. A 2009 report by the Korea Institute for Industrial Economics and Trade found that the competitiveness of eco-friendly automotive components’ materials only stands at about 70~80% compared to developed economies. In particularly, Korea is lagging in its ability to lead the commercialization of findings based on base technology to

develop materials for high-efficiency automotive components.

With countries around the world imposing stringent regulations on fuel economy by 2025, the transportation industry and the chemical materials sector also face a drastic change in their industrial environment. Accordingly, if the government fails to provide active support, Korea is expected to have to rely on imports of high value-added chemical materials. Considering shrinking yields in the domestic chemical industry that focuses only on conventional generalpurpose materials, it is deemed to be an urgent crisis situation.

If the government, however, plays an active and supportive role in R&D technology and successfully provides various programs to create an industry ecosystem, it is likely to secure global competitiveness in the transportation sector, as well as the domestic chemical materials & automotive parts industry.

What is the chemical materials/components industry for transportation?

The chemical materials/automotive components industry for transportation is an industry that manufactures and produces key interior and exterior parts for transportation, including automobiles, using chemical materials, such as plastics. The industry is divided into two categories: an industry that provides special functions to materials (materials/composites) and a mold manufacturing industry (molding/processing, parts/ modules, finished products). From the perspective of supply / value chain, it is generally created in a linear way: materials → composites and molding/processing → parts and modules → finished product.

The features of the industry ecosystem of the chemical

materials/components for transportation

There are about 3,300 manufacturers in the chemical industry for transportation, in which the amount of production is approximately KRW31 trillion and about 110,000 people are employed. The chemical materials/components industry, which is one of the largest industries, accounts for 5.6%, 2.8%, and 4.7% of the total manufacturing sector, respectively, thus having a significant influence on the domestic industry. Among 3,300 manufacturers, there are about 2,420 ones in the composites and molding/processing field, amounting to about 75%; there are about 880 companies in the parts and modules area, representing about 27%, which are mostly composed of SMEs and middle-standing firms. Accordingly, the average operating profits are only 5.3% and the average ratio of R&D investment remains at a disappointing 1.6%. Furthermore, excluding materials sectors, the remaining fields are closely related, serving as first tier, second tier, and third tier subcontractors, respectively, of transportation manufacturers/ producers. For example, manufacturers for parts and modules mostly server as first tier subcontractor and producers for composites and molding/processing act as second and third tier subcontractors. The distribution of subcontractors by region indicates that they are closely located at the transportation manufacturers/producers, representing 34% in the metropolitan area, 29% in the Southeast area, 13% in the Daegu-Gyeongbuk area, and 11% in the Honam area. From the perspective of value chain, the details are as follows:

Chemical materials

Chemical materials are a capital-intensive process industry mostly led by large companies, serving to produce low valueadded chemicals for general purpose or high value-added high-performance chemical materials. Barriers to entry into the market are generally high, and compared with technological competitiveness from developed economies, general-purpose resin accounts for more than 95% of the total chemicals, gaining excellent technical skills. However, the highperformance engineering plastics industry is about 70%. In Korea, there are 10 suppliers, including Kolon Plastics Inc, GS Caltex Corporation, and LG Chem, Ltd.

Composites and molding/processing

This industry is a labor-intensive industry mostly led by small and medium-sized enterprises (SMEs). Depending on the level of difficulty, about 2,400 firms make various products in small quantity. The industry is mainly in the form of simple toll processing, with lower barriers to entry in the market: its technical skills are regarded as about 70~80%, compared with developed economies.

Parts/modules

This industry is a labor-intensive process industry mostly led by large companies and middle-standing firms. It has similar structure to composites and molding/processing, but about 880 manufacturers specialize in specific goods. With higher barriers to entry in the market, its technical skills are about 80% compared with advanced countries. Domestic suppliers include Hyundai Mobis, Han IL E-Wha Co., Ltd., and Duckyang Ind, Co., Ltd.

Finished products

This industry is a technology-intensive process industry mostly led by large companies, serving as manufacturers/producers for transportation (passenger cars, railroad cars, and so forth). Its suppliers include Hyundai-Kia Motors and Renault Samsung Motors Co., Ltd.

The market-size and prospects for the chemical

materials/components industry for transportation

The global market size of the chemical materials/components industry for transportation is expected to reach KRW1,450 trillion in 2025, rising from KRW 310 trillion in 2012.

It is forecast to register over double digit growth driven by the growth of the transportation market and an increase in the rate of chemical application.

– The global market size: KRW310 trillion (2012), KRW737 trillion (2018), KRW1,450 trillion (2025)

– The rate of chemical application: 8% (2012), 15% (2018), 30% (2025)

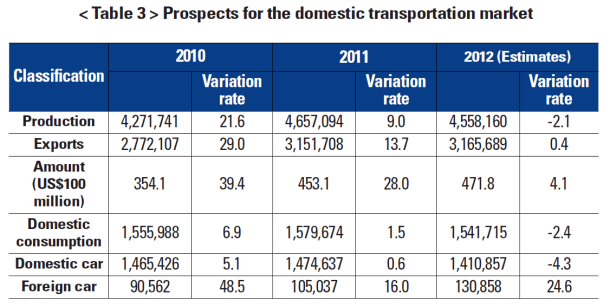

Contrary to global market trends, in the domestic market, the growth of production, domestic consumption, and exports is on the decline in the domestic transportation market, which is an end market, so it is expected to reach its limits if the existing strategy is the only method. On the production and domestic consumption front, it registered a negative growth in 2012 due to shrinking consumer confidence; exports growth also declined markedly.

By contrast with the global market, the domestic chemical market size for transportation is expected to register KRW69 trillion in 2025, rising from KRW18 trillion in 2012. It is true that there is a growing demand for the application of high stiffness and lightweight chemical materials to transportation vehicles. However, considering that the level of technology of domestic chemical materials falls behind that in developed countries, overseas chemical companies are likely to mostly occupy the market demand from Korea. Under the circumstances, an effective related strategy is urgently needed.

– Production: KRW18 trillion (2012) KRW35 trillion (2018), KRW69 trillion (2025)

– Export: KRW13 trillion (2012) KRW25 trillion (2018) KRW48 trillion (2025)

– Employment: 85,000 persons (2012), 166,000 persons (2018), 324,000 persons (2025)

– Added value: KRW5.2 trillion (2012), KRW10.2 trillion (2018), KRW20.0 trillion (2025)

Technological convergence among different industries, such as the transportation industry and the chemical sector, produces creative added value with high-risk and high profit. It requires longer time and higher costs, so it is hard for the private sector to take the lead in such investment projects.

Accordingly, it is necessary for the government to provide policy support.

The characteristics and weaknesses of the related industry in Korea

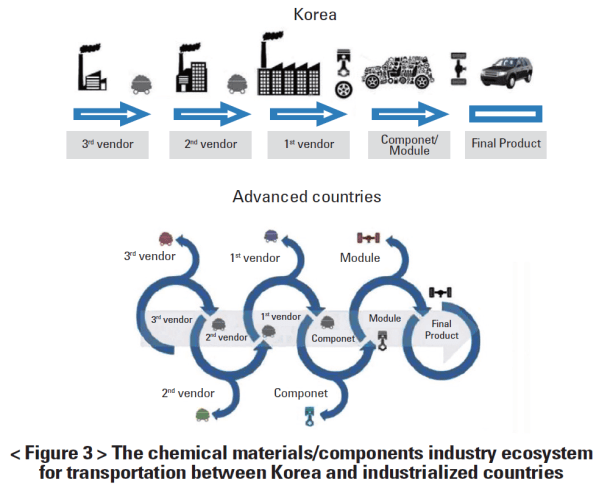

Industrialized countries now have a virtuous circle in an ecosystem of the chemical materials and the auto industry, while Korea has a linear ecosystem that focuses on specific companies in demand. Accordingly, suppliers are not diversified and fail to obtain sufficient technological skills, so they tend to depend largely on domestic companies in demand. This indicates that it is likely to have a poor growth base.

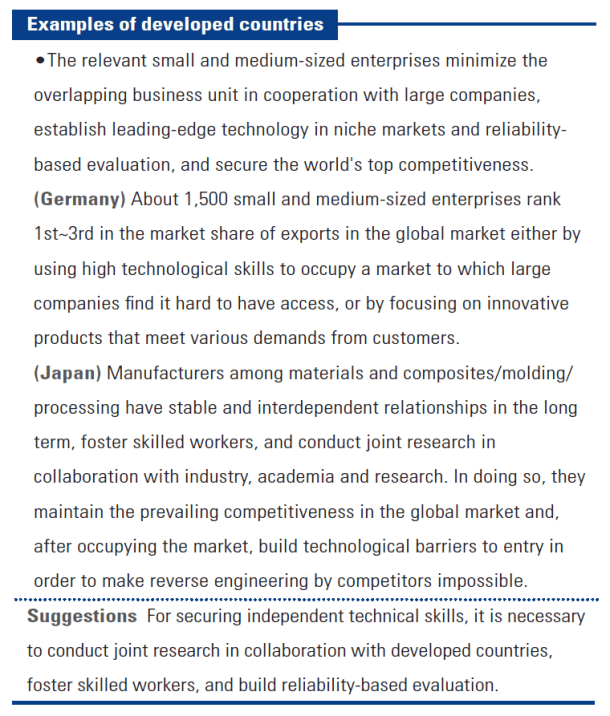

The analysis for the problems of the industry ecosystem for transportation is made by the value chain, and the examples of developed countries and suggestions are summed up as follows:

Chemical materials

Korea has secured technological skills in general-purpose chemicals, vying with global companies. However, the huge cost of technological development and the uncertainty of securing the market discouraged investment, so it lacks in the manufacturing and processing technology of original materials compared with advanced economies countries. For instance, the current status of the application to domestic transportation vehicles by alternative chemicals in developed countries finds that Nylon 66, typical engineering plastics, represents 80% (Rhodia, the United States), polyacetal resin, which is generalpurpose engineering plastics, accounts for 64% (KEP, the United States), ployphenylene sulfide, heat resistant hyperplastics, 52% (Toray, Japan), and other engineering plastics, such as MPPO and fluoride resin, 100% (Dupont, the United States). Up until now, special upgraded engineering plastics in Korea are relatively falling behind other developed countries, thus making it difficult for related Korean companies to develop and supply chemical materials for transportation.

In addition, the production of high functional chemicals, which account for more than 30% of the market share in the domestic chemical industry for transportation, is currently discontinued and, due to the lack of communications with companies in demand and joint research, the development of demand-based materials is not yet made. Thus, the analysis suggests that manufacturers of chemical materials lack product information from companies in demand.

Composites and molding/processing

This industry is regarded as a 3D industry, although it has a core ecosystem in the value chain of transportation. Researchers in the analysis point out that there is lack in technology arising from a shortage of skilled workers for research and production technology, as well as poor reliability assessment. In other words, first-tier subcontractors, which are small and medium-sized firms, find it difficult to obtain the durability of new materials and compounded components due to expenses. They also have difficulties in introducing specific production facilities or analysis equipment. In addition, secondtier subcontractors, which are typically regarded as 3D industries, lack in molding and processing technologies, so they are mainly dependent on first-tier subcontractors. Some small and medium-sized companies with technical skills were taken over by large firms. In other cases, shrinking business areas from the expansion of business units by large companies undermine the independent growth.

Parts/modules

The parts and modules industry has vertical and dependent relationships with transportation vehicle manufacturers and producers, and is influenced by their demands. In many cases, such industry is operated as a specialized company. Accordingly, the industry finds it difficult to enter the ecosystem market as a new entrant, has poor global marketing, and, when it makes a deal for the price of products, is in a disadvantageous position due to single suppliers. This leads to low profits, undermines investment in technology development, and in turn, aggravates the development of key components. This vicious circle results in lower technology than foreign parts makers.

In some cases, the industry cannot rely on the quality of products self-developed by composites and molding/processing manufacturers. When problems occur, companies in demand do not want to apply such products because of poor ability to respond to the problems. Automobiles, particularly, have a short development cycle, so it is fair to say that they have no ability to apply the above self-developed products.

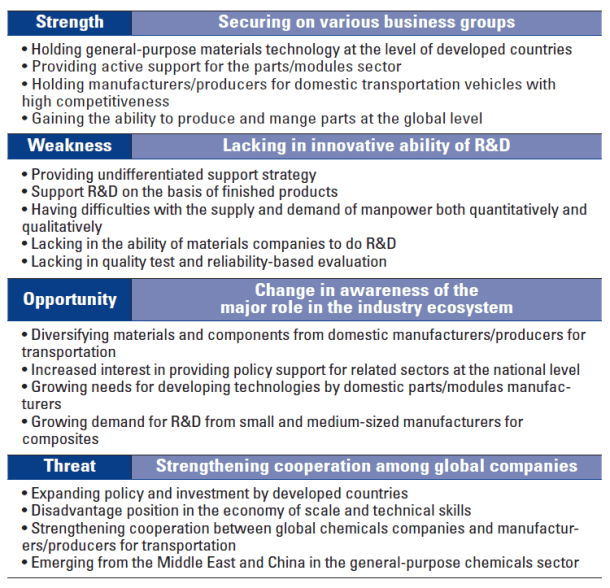

Analysis of related industries

Previously, this issue explored the analysis of value chain in the entire industry for transportation vehicles and resulting suggestions. Based on such analysis, it presented the strengths and weaknesses of the chemical materials/components industry for transportation in Korea. The industry is expected to continue to grow in the future, because it has business groups with various technologies and there is growing demand from the global market. However, this industry has its own weakness: it lacks the innovative ability to do R&D, has poor reliability evaluation, and is weak at exploring sales channels. So this will hinder the growth of such manufacturers.

Based on SWOT analysis above, the policy directions for promoting the chemical materials/components industry for transportation are explored and the results are as follows: First, there is a need to foster global middle-standing companies and develop innovative products in order to build close connection with the industry in demand and improve the reliability of the components of alternative chemicals. Second, with the aim of improving quality in response to the demand, it is necessary to strengthen the base that makes it possible to develop original processing technology and practical technology. Third, based on technology, the policy is required to maximize the sales channels and marketing capacity through diversified suppliers.

Fourth, focusing on small and medium-sized enterprises, there is a need to attract excellent researchers and cultivate technical talents necessary for industrial demands.

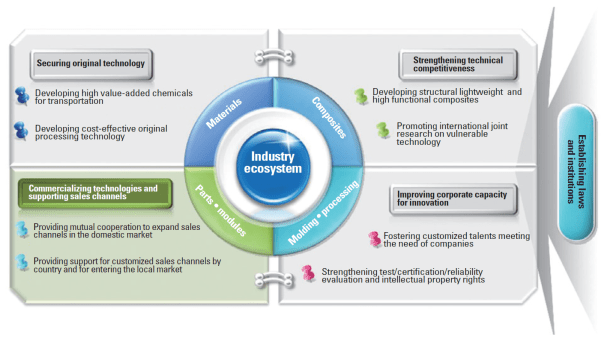

Basic policy directions

With the aim of establishing a virtuous circle where the chemical materials/components industry for transportation builds cooperative relations for workforces, technical reliability evaluation, and sales channels, the Korean government carries out strategies by securing original processing technology, strengthening technical competitiveness, commercializing technologies, providing support for sales channels, improving corporate capacity for innovation, and establishing laws and institutions.

① Reinforcing support for international joint research on vulnerable technology areas and for securing low-cost processing technology by using the existing R&D supporting system→securing world-class technology

② Fostering the flow of new and excellent workf orce, establishing a re-training system for on-site technical talents, and building test/reliability based evaluation→improving corporate capacity for innovation

③ Providing support for promoting mutual growth with companies in demand, for exploring customized sales channels by country, and for entering the local market→commercializing technologies and establishing a supporting system for sales channels

④ Providing support for specialized complex, improving employment environment, and providing support for establishing mutually shared infrastructure→establishing laws and institutions

• To specify policy directions, it is necessary to focus on three goals: developing low-cost (↓20%) chemicals for transportation, fostering 10 small hidden champions, and creating a virtuous circle of industry ecosystem.

Process plan for building an industry ecosystem of

plastic-based chemical materials for transportation

Establishing development system for lightweight/ functional and eco-friendly technology

In Korea, the chemical materials industry focuses on developing and producing general-purpose chemical materials. Serving as a national basic industry, the industry has achieved technological competitiveness to the point of vying with global companies through various R&D activities. However, the high value-added chemical sector, such as supper engineering plastics, is in a technologically disadvantageous position compared to global companies, so it depends on imports of such materials.

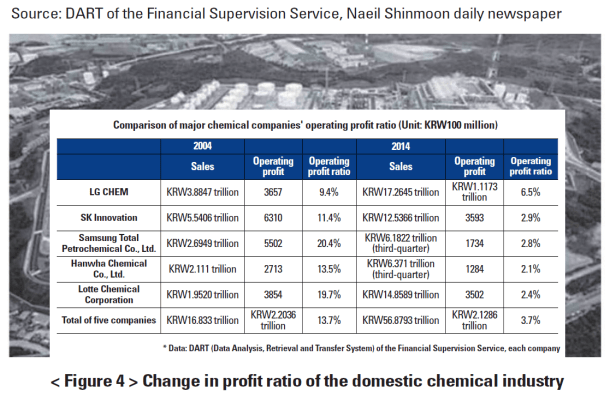

Currently, the change in operating profit ratio of the Korea’s top-five chemical companies suggests that the ratio has declined to about a quarter over the past ten years, leading to shrinking profits. This results from the domestic petrochemical industry’s concentration on general-purpose materials. If the industry fails to depart from industrial structure that centers on generalpurpose materials, it is expected to face limitations to growth in the near future.

In addition, there is an oversupply of general-purpose materials across the world due to an increase in production by China, which was once in a technologically disadvantageous position against Korea, and the Middle East, which holds an advantageous position as an oil-producing country. This increasingly leads to a shrinking growth rate in the domestic chemical materials industry and causes the industry to have less influence on the global market. With the domestic transportation industry and each country imposing stringent regulations on fuel economy and CO2, lightweight/ functional and eco-friendly factors are increasingly essential for survival. Most of all, to resolve problems with fuel efficiency (air pollution), there is a growing demand for lightweight-related research. Generally, the ultimate way to improve fuel efficiency is to enhance the performance of power engines. However, in terms of efficiency, automobile manufacturers make efforts to develop technologies that make it possible to use materials that reduce vehicle weight and substitute metal parts by developing highperformance plastics with the features of high-tensile strength and high-thermal stability. Under the circumstances, in line with a strong base in the domestic chemical materials industry, the trend in finished car makers toward lightweight vehicles, and the demand for high-functional materials, the development of high functional and value-added plastic materials, which substitute metals, will drive a new growth engine for the domestic chemical materials industry.

Depending on the availability of crystalline in internal chemical structure and continuous use temperature, plastic materials are subdivided into three sections: standard; engineering; and highperformance plastics. High-performance plastics are the general term, including high temperature and high-tensile strength plastics with continuous use temperature of over 150℃. They typically include Polysulfone (PSU), Polyethersulfone (PES), Polyetherimide (PEI), and Polyphenylenesulfide (PPS).

Unlike plastic materials for general use, high-performance plastics feature high continuous use temperature and excellent mechanical properties. Most of all, PPS consists of phenyl and sulfides, has a high melting point of about 280℃, and has an excellent high thermal stability with continuous use temperature of 200~240℃. Owing to low coefficient of linear thermal expansion and flame retardant and high chemical resistance, and mechanical properties, PPS has recently gained attention as a material for transportation and electric and electronic parts. In addition, PPS has the highest growth rate among highperformance plastics and due to the expansion of electric cars, demand for it is expected to grow continuously in the future.

Source: The current status of market trend and development of SK Chemicals Co., Ltd., 2014

Korea once depended solely on imports of PPS base resin, but in recent years, it has established a foundation for producing PPS base resin that is more eco-friendly and economic base resin than the conventional method used in Japan and the United States through the development of the domestic new polymer processing. Compared with the conventional solution processing that used sodium sulfide, this polymer processing is a melting processing method that directly uses sulfide, which provides not only the minimized content of chlorine but also excellent costeffective properties, compared to the conventional processing.

High-performance plastics can substitut various components to which metals only applied in the transportation and electrical/ electronics industry, so the development of high-performance plastics will provide an opportunity for the application of lighter materials with low costs. For instance, functionally high thermal stability resin will be developed with the features of dimensional stability, electrical properties, and radiation resistance. If such resin is substituted with metal materials that are applied to the module of automobile headlamps, this is expected to achieve a reduction of more than 30% for lightweight vehicles. The compounding of chemical materials enables the application of materials with high thermal stability and high tensile strength to automotive engine peripheral parts. So it is expected to substitute metal materials.

To materialize such technologies, the domestic chemical materials industry makes various efforts to develop eco-friendly raw materials for high tensile strength and high thermal stability to ultra-light and functional composite materials using organic and inorganic materials, as well as material processing and molding technologies. Among 14 tasks from industry engine projects, the industry first promotes seven technology development tasks, considering the urgency and redundancy as below, and plans to carry out the remainder of tasks.

Conducting joint international research for completing domestic vulnerable technology

To make up for vulnerable technologies in Korea, the related industry plans to conduct joint international research with universities, research institutes, and companies from technologically developed countries, such as the United States, Germany, and Japan, in order to shorten the R&D period. First of all, in the case of technology development task for 2014, this industry plans to create a synergy effect of R&D by systematically connecting the findings of basic research from the United States with applied research from Korea in research collaboration with Florida International University and Northeastern University in the United States. It will promote joint R&D of chemical materials for vehicles and the linkage of technological commercialization by establishing cooperative relations between domestic specialized institution of chemical materials and automotive cluster Thüringen under the development corporation of Thuringia (LEG Thüringen) consisting of 114 companies, universities, and institutions, including BMW and MITEC.

<Ceremony for establishing international cooperation

for industry growth engines on Dec. 29, 2014>

Strengthening the linkages among technological development ecosystems

To operate effective projects at the government level, share accomplishments, and secure the linkages among industry ecosystems, such as materials, parts, and modules, the related industry plans to promote and operate polymer materials research association. The research association will see the participation of automobile materials, processing and parts makers to reinforce industrial value chains. The United States, for instance, created the Society of Plastics Engineers Automotive Section consisting of researchers in the fields of material processing (molding), equipment, and finished cars to strengthen the linkages among industry ecosystems.

Fostering a highly skilled workforce to meet industrial demand and reinforcing capacities of on-site workforce

The industry plans to actively provide support for cultivating highly skilled human resources (advanced degrees) that could meet the demand of companies by linking the education project of materials and parts’ workforce, promoting retraining of on-site technical staff, and smoothly supplying manpower to the chemical industry. By using specialized education systems, such as material & convergence graduate school, it will foster human resources with advanced degrees who meet the demand of plastic composites-related companies. In addition, it plans to provide education by creating new training curriculums for the sectors of new processing processes, processing simulation, extrusion & injection precision engineering, and molding analysis, in which are very short of human resources, and by making use of outside instructors with their specialties, except full-time professors from universities.

To nurture on-site technical manpower, it will create new curriculums for on-site technical manpower of SMEs and middlestanding firms that intend to participate in “the development of plastic composites,” and offer training by making use of experts from participatory research institutes (Korea Research Institute of Chemical Technology, the Korea Automotive Technology Institute, etc.). Based on difficulties that engineers experienced in the workplace, it will provide short-term training for the latest technology, seminars, and joint workshops.

Building basis for testing, certification and reliability evaluation and the management of intellectual property rights

To succeed in the development and commercialization of materials and parts, there is an urgent need to establish support infrastructure for producing a prototype connected with analysis and molding, for evaluating reliability of testing and certification, and for managing intellectual property rights. For technology development companies to receive full support for prototyping production and testing evaluation, the related industry is considering support for infrastructure in areas, such as the central, southeastern, and southwest regions, given regional industrial placement and the network of technology development. With regard to intellectual property rights, it plans to promote support for IPR in connection with IP management, IP Pool membership service subscription, and IP-R&D strategy support project.

Conclusion and suggestions

In Korea, the chemical materials industry focuses on producing general-purpose materials, so this puts the country in a difficult situation when it swiftly responds to the competition with China and the Middle East for the market share. Since the chemical materials industry is a large-scale process industry, it is difficult for companies to change conventional materials into new ones. In the case of the transportation industry, which is a core national industry, it of course serves as a driving engine for economic growth. Due to stringent environmental regulations from each country, this urgently requires the industry to develop new materials.

However, companies in the domestic chemical materials industry are in a poor position in regard to their technical skills, so the domestic chemical materials industry for transportation is likely to expect to gradually lose market share.

To maintain the competitiveness in the chemical materials and the transportation industry in Korea and expand the market share in the global market, an integrated approach needs to be taken in order to secure the soundness of the industry ecosystem, rather than simple support for technological development. In other words, based on the global trends and future market prospects, a virtuous cycle in an industry ecosystem should be created where SMEs and middle-standing firms from diverse sectors and classes can pursue mutual growth by clearly establishing the direction of technological development in the chemical materials and the parts industry, fostering human resources for industrial demands, building infrastructure for providing support for companies, and offering support for technical commercialization and tax benefits. As for the research and development, the chemical materials industry has to focus on lighter, smarter, more eco-friendly chemical materials. This will make companies substitute metals with new materials, and improve the performance of components. If materials that are not harmful to humans are developed, this will likely pave the way for taking the lead in the marketplace, as well as meeting needs from the global market. In addition, along with various institutional support for improving research and corporate conditions of domestic SMEs and middlestanding firms, which represent more than 80% of the chemical

and materials industry, training programs are developed to directly help people in the on-site workplace. So it will act as an opportunity to improve capabilities in the industry ecosystem.

korean-machinery.com | Blog Magazine of korean-machinery, brands and Goods